Two quotes land in your inbox for the same car. One is 4,000 rupees cheaper. Easy choice, right? Then your car gets rear-ended six months later, the cheaper insurer drags the claim out for three weeks, the nearest cashless garage turns out to be 40 kilometres away, and depreciation deductions drain a third off your payout. That 4,000 rupee saving just became a very expensive lesson. Well, the trick to buying a car cover is knowing that the premium is only one number on a long list of numbers that matter.

Learning to compare car insurance properly is less about hunting for the lowest price and more about reading the whole picture: what gets paid, how fast, where, and with how many deductions. Get that right, and you spend the same money on a policy that actually shows up when you need it. Here is exactly how you can compare car insurance plans in India to find the one that unlocks maximum savings.

Beyond Premium: Things To Compare When Shopping for Car Insurance

Premium is the loudest number, so it often grabs all the attention. However, the problem here is that the cheapest premium often hides a thinner safety net. A proper car insurance comparison in India weighs five things together and not just one. These include:

- Claim settlement ratio: the share of claims the insurer actually pays. Above 90% is reliable, and the closer to 98%, the better.

- Cashless garage network: how many garages near you let the insurer settle the bill directly, so you pay nothing upfront beyond your deductible.

- Insured Declared Value: the agreed market value of your car, which decides your payout in a total loss or theft.

- Add-on range and cost: zero depreciation, engine protection, roadside assistance, and what each insurer charges for them.

- Claim speed and service: a high ratio means little if settlement crawls, so reviews about turnaround matter.

When you compare car insurance on these five parameters together, the picture changes completely. An insurer that is 3,000 rupees dearer but pays in 48 hours through a garage near your home can be far better value than the cheapest quote on the screen. Price tells you what you spend. The other four tell you what you actually get.

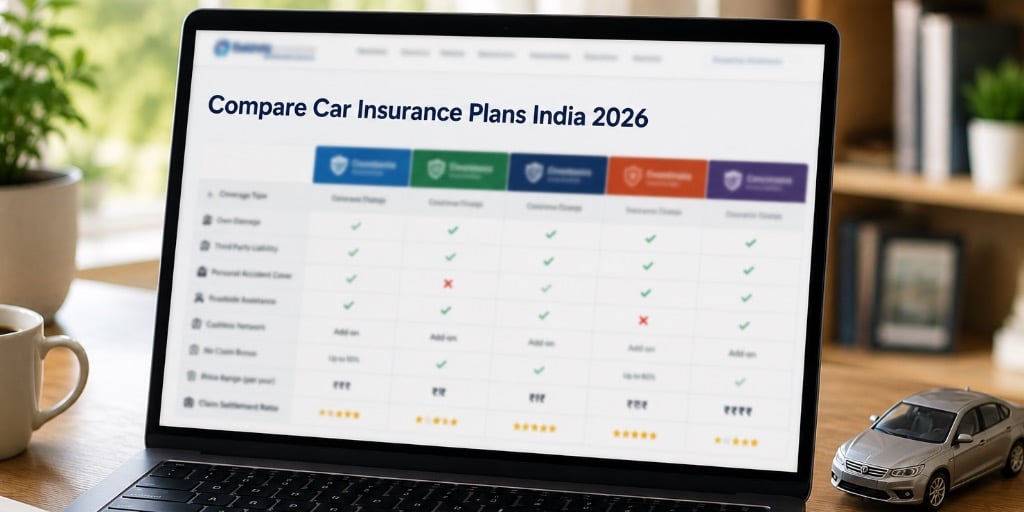

How to Read a Car Insurance Comparison Table

A car insurance comparison table is only useful if you know which columns deserve your attention. Faced with a row of quotes, most people scan straight to the premium and stop. That is exactly the wrong instinct.

| Premium Quoted | IDV Offered | Cashless Garage Count | Claim Settlement Ratio |

| Insurer 1 | Rs. XX | XX | X% |

| Insurer 2 | Rs. XX | XX | X% |

Start from the right of the table, not the left. Look first at the claim settlement ratio, then the cashless garage count in your city, then the IDV each insurer is offering, and only then the premium. Reading it this way forces you to judge value before price. Two quotes with the same premium can differ wildly if one offers a fair IDV and a dense garage network while the other quietly lowballs your IDV to make the premium look attractive. A smart car insurance comparison in India treats the premium as the tiebreaker between strong options, not the headline that decides everything.

Watch for two common traps. First, a suspiciously low premium, which often means a deflated IDV, which shrinks your payout when you can least afford it. Second, identical-looking plans that may include different add-ons. Make sure to compare before you judge the price.

Premium Comparison: Same Car, Different Insurers

Since the third-party portion of your car insurance premium is fixed by IRDAI and is identical across every insurer, there is essentially nothing to compare there. The table below shows the latest TP premium rates by engine capacity, exclusive of GST:

| Engine capacity | Fixed annual third-party premium |

|---|---|

| Up to 1000cc | Around 2,094 rupees |

| 1000cc to 1500cc | Around 3,416 rupees |

| Above 1500cc | Around 7,897 rupees |

Beyond the TP premium, everything else is where insurers truly compete. The own-damage premium, typically a few per cent of your IDV, varies meaningfully between companies for the very same car. Two insurers quoting on an identical 1200cc hatchback with the same IDV can differ by several thousand rupees once their own-damage pricing and bundled add-ons are factored in. This is the single biggest reason to compare car insurance before you buy rather than renewing on autopilot. The mandatory part is fixed for everyone, but the optional part, which is most of your bill, is yours to shop around.

Picture a real example. Say two insurers, A and B, both quote on a 1200cc hatchback with an IDV of 5.5 lakh rupees. Insurer A quotes a comprehensive premium of 11,000 rupees with zero depreciation bundled in. Insurer B, on the other hand, quotes 9,500 rupees but without zero depreciation, charging 2,000 rupees extra to add it.

Glance at the headline, and B looks cheaper. Add the rider you actually want, and B costs 11,500 rupees, more than A, for the same protection. This is the kind of eye a careful car insurance comparison in India requires. The lesson repeats across almost every comparison: the cheapest first number is rarely the cheapest final number.

Claim Settlement Ratio: What Each Percentage Point Means in Practice

The claim settlement ratio is the number that separates a real promise from a sales pitch. It is the percentage of claims an insurer pays out of those filed, and small differences carry real weight.

Think of it in human terms. An insurer at 98% rejects or disputes roughly two claims in a hundred. One at 85% disputes fifteen. If you are unlucky enough to be one of those fifteen, the lower ratio stops being a statistic and becomes your problem. This is why a ratio above 90% is the floor any serious car insurance comparison in India should insist on, and why the leaders sitting near 98 to 100% earn the trust.

But the ratio itself also has a blind spot. It tells you whether claims get paid, and not how quickly they are paid. Some insurers settle in-network cashless claims within 48 hours, while reimbursement claims at out-of-network garages can take 15 to 30 days across almost every company. So pair the ratio with two checks: how fast the insurer settles cashless claims, and whether your preferred garage is in its network. A high ratio plus slow service still leaves you without a car to drive for weeks.

Cashless Garage Network: Why Count and Location Both Matter

A big garage number on a sales page might look reassuring. But what matters far more is whether even one of those garages sits near where you drive. A network of 16,000 garages is useless to you if the one nearest to you is in another district.

Cashless garages are the ones the insurer has tied up with, so when you repair there, the insurer pays the garage directly, and you cover only your deductible and any excluded items. The alternative to this route is to get a reimbursement, which means paying the full bill upfront and waiting weeks to be paid back. That gap is exactly why location beats raw count.

When you compare car insurance, do not just note the total garage figure. Check the insurer's garage list for your own city and, ideally, the routes you drive most. Public sector insurers often have strong reach into smaller towns where private players are thin, while digital-first insurers may have dense metro coverage but sparse rural presence. The right answer depends entirely on where your car actually spends its time.

Add-on Comparison: Which Insurer Bundles Best and The Power of Zero Dep

Add-ons are where two policies that look identical on premium quietly diverge on value. The same three or four riders crop up again and again, and how an insurer prices and bundles them can swing your decision. Some of the most common add-ons you will encounter during your purchase include:

- Zero depreciation: a cover that ignores the depreciation deduction on replaced parts, paying the full part cost. The most valuable add-on for cars under five years old.

- Engine protection: covers engine damage from water ingress and oil leakage, vital in flood-prone cities.

- Roadside assistance: covers towing, fuel delivery, and breakdown help and is worth it for long-distance and highway drivers.

- Return to invoice: pays your car's original invoice price rather than the depreciated IDV on a total loss or theft.

Some insurers bundle these add-ons attractively, offering zero depreciation and roadside assistance together at a keen price, while others charge for each separately. A genuine car insurance comparison in India checks not just whether an add-on is available but what it costs and whether it is bundled. Two quotes with the same premium can deliver very different protection once you account for which add-ons are baked in. Always compare car insurance on the cover you will actually use, not the cover that simply makes the brochure attractive.

When choosing between add-ons, make sure to pick zero depreciation. In an ordinary claim, the insurer deducts depreciation on replaced parts, and plastic and rubber components often depreciate faster. On a claim involving a bumper, fender, and a few panels, that deduction can quietly cut your payout by a third or more. Zero depreciation wipes out that deduction and pays the full part cost, which is why it pays for itself in a single decent claim on a newer car. When you compare car insurance for a vehicle under five years old, the presence and price of this rider should weigh almost as heavily as the base premium itself.

Why a Comparison Platform Beats Quoting One Insurer at a Time

Visiting each insurer's site one by one is not just time-consuming, but it also makes a fair comparison almost impossible. By the time you reach the third quote, you have forgotten what IDV and add-ons the first one assumed. An insurance comparison website in India solves this by putting every quote on the same terms, side by side, so you are judging like with like.

The value of a good insurance comparison website in India is not just speed. It is the consistency. When the same car, the same IDV, and the same add-ons feed into every quote, the differences you see are the real differences in insurer pricing, not artefacts of mismatched inputs.

That is the only way to spot which company genuinely offers the best car insurance comparison outcome for your situation. An online comparison platform also surfaces claim settlement ratios and garage networks next to the price, which a single insurer's own site will never do, because no insurer wants you looking at a rival who pays faster. This is why the best car insurance comparison habit starts with a neutral platform rather than a brand's own quote page.

How to Complete a Car Insurance Purchase After Comparing

Once your comparison points to a winner, finishing the purchase online takes minutes. The path is straightforward, and here is what you need to do:

- Enter your car make, model, variant, and registration details on your chosen platform or insurer site.

- Set a realistic IDV, neither inflated nor lowballed, so your payout matches your car's true value.

- Select your cover type and the add-ons your comparison identified as worth buying.

- Apply your No-Claim Bonus, which carries over from your previous policy if you renew on time.

- Review the final quote against the rivals one last time to confirm it still wins.

- Pay online and download the policy document instantly.

Once paid, keep a digital copy on your phone or DigiLocker, since a digital insurance copy is also valid proof of insurance. The whole insurance purchase process usually wraps up in well under fifteen minutes once you have done the comparison groundwork. The effort you put into the comparison is what makes this final step feel easy and confident rather than a gamble.

Car Insurance Comparison: Making The Smart Move

Comparing car insurance is not about chasing the lowest premium. It is about reading the whole page, claim ratio, garage network, IDV, add-ons, and service, and letting price settle the contest only after the value is clear. Do that, and the policy you buy will be the one that turns up quietly and quickly on the worst day of your driving year, which is the only test of car insurance that ever really counts. Take fifteen minutes to compare properly now, and you save yourself weeks of frustration later.

Note: This article has been vetted by Siddarth Khandelwal, an Insurance expert at Insure24.

FAQs

Q. How to compare car insurance plans India buyers can trust?

Compare five things together: claim settlement ratio, cashless garage network in your city, the IDV offered, add-on cost and bundling, and claim speed. Treat premium as the tiebreaker between strong options, not the headline. This balanced approach beats picking the cheapest quote every time.

Q. What is the best car insurance comparison site India offers?

The best car insurance comparison site in India 2026 is one that shows multiple IRDAI-regulated insurers side by side on identical cover, lets you adjust IDV and add-ons, and displays claim settlement ratios. Insure24 lets you compare car insurance across insurers on one screen so you can judge value, not just price.

Q. Is the cheapest car insurance plan the best choice?

Rarely. The cheapest premium often hides a deflated IDV, a thin garage network, or slow claim service. A proper car insurance comparison in India weighs what you get against what you pay, since a slightly dearer plan that pays fast through a nearby garage is usually better value.

Q. Does the third-party premium differ between insurers?

No. IRDAI fixes the third-party premium by engine size, so it is identical across every insurer. When you compare car insurance, the differences lie entirely in the own-damage premium, the IDV, the add-ons, and the service, which is where your shopping around pays off.

Q. How do I do a car insurance compare online in India the right way?

Get quotes for the same car, IDV, and add-ons from several insurers on one platform, then read the table from claim ratio and garage network first, premium last. A car insurance compare online in India done this way takes minutes and surfaces the best value rather than just the lowest number.

Q. How does IDV affect my comparison?

IDV is the agreed value of your car and the maximum payout on a total loss or theft. A lowballed IDV makes a premium look cheap but cuts your payout, so always compare quotes at the same realistic IDV. Otherwise, you are comparing two different levels of protection.

Q. Should I compare comprehensive car insurance or stick with third-party?

For most cars with meaningful resale value, compare comprehensive car insurance, since third-party covers only damage to others and nothing for your own car. Third-party alone suits only very old, low-value cars where own-damage cover is no longer worth the premium.

Q. How often should I compare and switch insurers?

Once a year at renewal is ideal. Premiums, garage networks, and service levels shift, and your No-Claim Bonus carries over when you switch, so there is no penalty for changing. A quick annual comparison ensures you never overpay out of habit.

Q. Why do two insurers quote different premiums for the same car?

Because the own-damage premium is set by each insurer based on their pricing, your IDV, your city, and the add-ons bundled in. The third-party portion is identical, but everything else varies, which is exactly why a side-by-side comparison reveals real savings.

Q. Is buying car insurance online after comparing safe?

Yes, provided you buy through an IRDAI-regulated insurer or a licensed platform. Digital KYC and regulatory oversight make online purchases secure. Confirm the site is authentic, and you get instant policy issuance with a valid digital document by email.

Q. What documents do I need to compare and buy car insurance?

Very few. To compare car insurance, you mainly need your car's make, model, variant, and registration details, plus your previous policy number for the No-Claim Bonus. The purchase itself is paperless on most platforms, with digital KYC replacing physical documents.

Q. Can I compare car insurance for an electric car the same way?

Yes, with one difference. Electric cars have no engine cubic capacity, so their third-party premium is based on battery power in kilowatts rather than cc, and they often attract a discount. Everything else, such as claim ratio, garage network, IDV, and add-ons, compares the same way.

Licenced by

COMPANY

PRODUCTS

RESOURCES

LEGAL

Cars24 Financial Services Private Limited

(Wholly owned subsidiary of Cars24 Services Private Limited)

Corporate Office - 6th Floor, SAS Tower-C, Ch Baktawar Singh Road, Medicity Sector 38, Shivaji Nagar,

Gurgaon - 122001, Haryana

IRDAI Corporate Agency Registration No: CA0710 | License Category: Composite |

CIN: U65990HR2018PTC075713

Disclaimer : The information contained in this website is presented purely for information purposes only provided as service to the internet community at large. It does not constitute insurance advice and we do not guarantee the accuracy, adequacy or the completeness of the information contained here.

Licenced by

COMPANY

PRODUCTS

RESOURCES

LEGAL

Cars24 Financial Services Private Limited

(Wholly owned subsidiary of Cars24 Services Private Limited)

Corporate Office - 6th Floor, SAS Tower-C, Ch Baktawar Singh Road, Medicity Sector 38, Shivaji Nagar,

Gurgaon - 122001, Haryana

IRDAI Corporate Agency Registration No: CA0710

License Category: Composite

CIN: U65990HR2018PTC075713

Disclaimer : The information contained in this website is presented purely for information purposes only provided as service to the internet community at large. It does not constitute insurance advice and we do not guarantee the accuracy, adequacy or the completeness of the information contained here.